The Real Reason Google Gave Gemma 4 Away

Key Takeaways

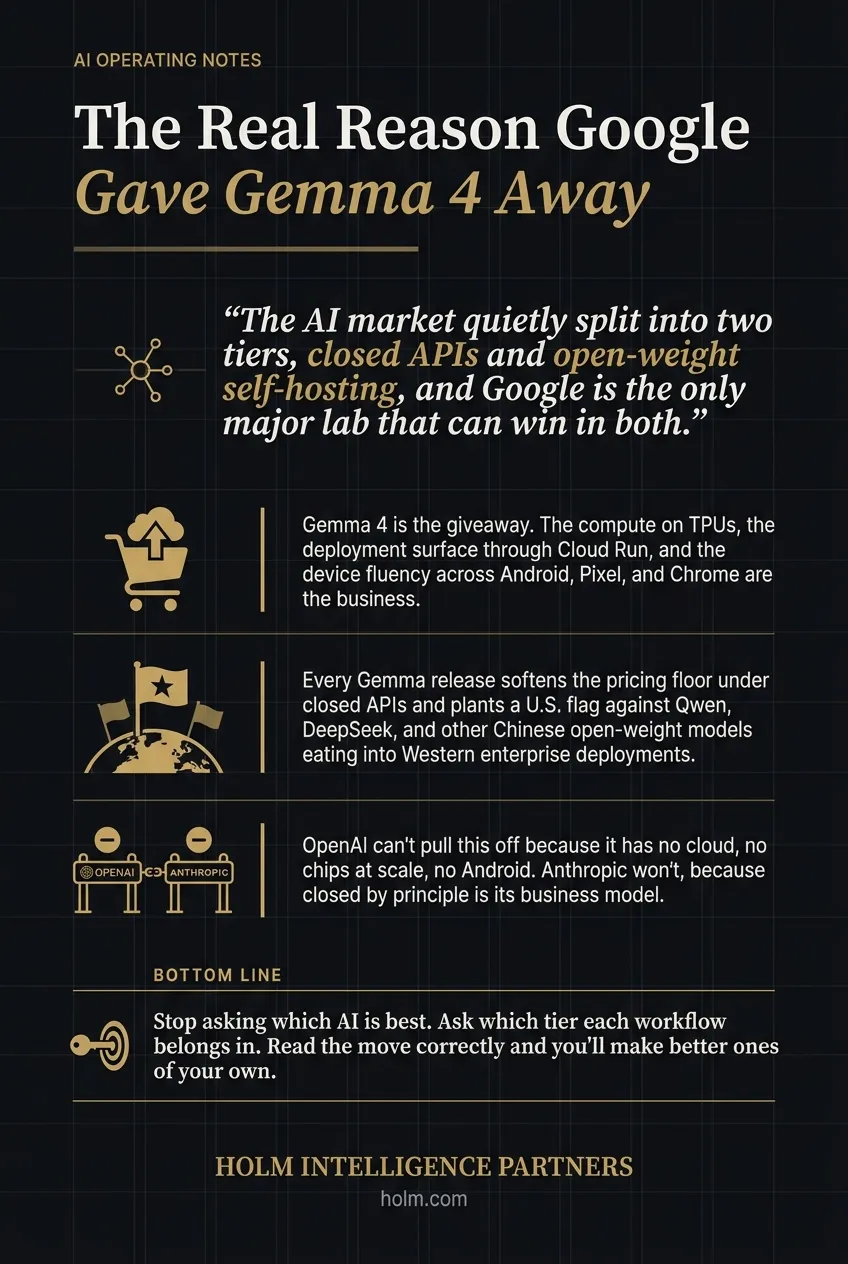

- The AI market quietly split into two tiers, closed APIs and open-weight self-hosting, and Google is the only major lab that can win in both.

- Gemma 4 is the giveaway. The compute on TPUs, the deployment surface through Cloud Run, and the device fluency across Android, Pixel, and Chrome are the business.

- Every Gemma release softens the pricing floor under closed APIs and plants a U.S. flag against Qwen, DeepSeek, and other Chinese open-weight models eating into Western enterprise deployments.

- OpenAI can't pull this off because it has no cloud, no chips at scale, no Android. Anthropic won't, because closed by principle is its business model.

- Stop asking which AI is best. Ask which tier each workflow belongs in. Read the move correctly and you'll make better ones of your own.

The Real Reason Google Gave Gemma 4 Away

Google didn't release Gemma 4 out of generosity. They did it because the AI market quietly split into two tiers, and Google is the only major lab that can win in both.

Most coverage of this release missed the point. The story isn't open-source goodwill. It's a calculated three-part play that only works because of Google's cloud, chips, and Android footprint. OpenAI can't pull it off. Anthropic won't. And Chinese labs are already eating into Western enterprise deployments while everyone else argues about benchmarks.

Here's what's actually going on.

What does it mean that AI has split into two tiers?

For two years after ChatGPT, there was effectively one way to use AI. Hit an API, pay per token, get an answer back. OpenAI, Anthropic, Google. That was the market.

A second tier has formed underneath it. Open-weight models you download, run on your own hardware or rented GPUs, control end to end. No API. No per-token bill. No vendor sitting in the loop.

This isn't a security debate. You can deploy closed models inside private cloud environments. The economics don't change. You're still paying per token, still depending on a provider's pricing, still operating on their infrastructure.

Open weights are different in kind. You own the file. Marginal cost collapses to electricity and hardware. At scale that can be 10 to 100 times cheaper. And the deployment keeps running even if the lab that built it disappears tomorrow.

When does self-hosting actually make sense?

Volume. That's it.

A startup spending $2,000 a month on API calls will stay closed because convenience wins. A company spending $2 million a month starts looking at self-hosting seriously. Airbnb already moved meaningful AI workloads from OpenAI to Qwen for exactly this reason.

The lineup now looks like this:

- Closed only: OpenAI, Anthropic

- Open only: Meta, DeepSeek

- Both: Google

Google is the single major lab competing in both lanes. Gemma doesn't cannibalize Gemini. It captures workloads Gemini was never going to win.

Payoff one: the model is free, the infrastructure isn't

Gemma 4 is free. Running it well isn't.

Google built Gemma 4 to sit inside its cloud stack. It serves on Google's own TPU chips. It deploys through Cloud Run. It plugs into their agent development kits. It offers sovereign cloud configurations for regulated industries.

The numbers behind that stack: Google Cloud did $17.7 billion in revenue last quarter, growing 48% year-over-year, with $240 billion in committed contract backlog. Every enterprise that standardizes on Gemma is a candidate to run it on Google infrastructure.

Then there's the device side. The smallest Gemma 4 variants run on phones, laptops, and browsers. That strengthens Android, Pixel, and Chrome against Apple Intelligence and Samsung's AI stack. We're talking about device systems and ad revenue measured in tens of billions.

The model is the giveaway. The compute, the deployment surface, and the device fluency are the business.

Payoff two: blocking the competition on two fronts

Why the Chinese open-weight wave matters

Over the last year, Alibaba's Qwen, DeepSeek, Moonshot, and Z.AI shipped open-weight models that rival GPT-5 and Claude in real workloads. For a Western enterprise wanting to self-host, the best technical option was starting to look Chinese.

Think about what that means in practice. A European bank fine-tuning on Qwen. A U.S. healthcare company running clinical workflows on DeepSeek. A government agency building internal tools on Chinese weights. That's a geopolitical problem, a procurement problem, and a national security problem at the same time.

If Chinese open-weight models become the default for Western enterprise self-hosting, Google loses developer attention and the cloud revenue that follows. Gemma 4 plants a Western flag with a U.S.-built alternative, enterprise assurances, and no ingestion of customer data for training.

Why this also squeezes OpenAI and Anthropic

OpenAI and Anthropic charge premium API prices. That only works as long as there's no close free alternative. Every Gemma release softens the pricing floor under closed APIs.

Google can absorb this. It doesn't depend on API token revenue. OpenAI and Anthropic do. That's the whole asymmetry.

Payoff three: Gemma sells Gemini

Gemma 4 is built on the same research foundation as Gemini 3. Every benchmark Gemma wins reinforces the perception that Gemini is excellent. The free model markets the paid one for free.

It also creates developer gravity. Gemma ships under Apache 2.0, which removes legal friction. Every fine-tune, tutorial, tool integration, and shipped product means another engineer fluent in Google's AI stack rather than Meta's or Alibaba's or OpenAI's.

This is the long game. The engineers learning Gemma today are the architects writing procurement recommendations in three years. Developer fluency converts into purchase orders. Always has.

Why don't OpenAI and Anthropic do the same thing?

They can't, and in Anthropic's case, they won't.

OpenAI doesn't have a cloud, doesn't have its own chips at scale, doesn't have an Android. The model is the business. Give it away and there's nothing left to sell.

But OpenAI has been pressured to the edge of the open tier. In August 2025 they released GPT-OSS under Apache 2.0. Four things forced it:

- The DeepSeek shock. In January 2025, DeepSeek's R1 roughly matched o1 at a reported training cost under $6 million. That wiped about $600 billion off Nvidia's market value in a single day, the largest single-day loss in U.S. market history. Sam Altman wrote on Reddit that OpenAI had been "on the wrong side of history" on open source.

- Enterprise leakage. Self-hosted workloads were leaving for Llama and Chinese models.

- Researcher drift. Capability researchers can't study closed models meaningfully, so they were moving to open weights.

- Political pressure. The Trump administration's July 2025 AI action plan explicitly endorsed open-weight models as geostrategic. Altman's framing of GPT-OSS as "an open AI stack created in the United States based on democratic values" mirrored the administration's language almost word for word.

Notice the shape of the release. GPT-OSS was positioned at o4-mini level, a clear tier below frontier. GPT-5, fully closed, shipped two days later. The follow-up GPT-OSS Safeguard was a narrow safety classifier. The pattern: open releases are always sub-frontier, narrowly scoped, or both.

Anthropic has gone the other way. They've never released an open-weight model and are moving further into restricted access. Claude Mythos, announced April 2026, reportedly identified thousands of security vulnerabilities across major operating systems and browsers, some undiscovered for decades. Anthropic judged it too dangerous to release publicly. Under Project Glasswing, access is limited to roughly 50 vetted organizations chosen because the rest of the internet depends on their systems.

The reason researcher pressure doesn't hit Anthropic the same way is simple. The research community is split. Capability researchers need open weights, and OpenAI was losing them. Anthropic was never going to win them anyway. The safety and alignment community works through API access, red-team agreements, and published interpretability research. That's the community Anthropic actively built through fellowships and its published constitution.

The split is permanent

Each lab's tier choice is locked in by its business model:

- Google: both tiers, funded by cloud

- OpenAI: closed by default, with scoped open releases when pressured

- Anthropic: closed by principle, with restricted-access models for high-stakes use

- Meta: aggressively open, funded by ads

- Chinese labs: open as a global market-entry strategy

Stanford's tracking shows the capability gap between the best closed and best open models narrowed dramatically through 2024 and 2025, briefly hit parity, then widened back to about three points as closed labs pulled ahead. The lead has changed hands multiple times. That's a healthy two-tier market, not a winner-take-all race.

What this means for how you actually decide

Most leadership teams I talk to are still asking the wrong question. They're asking "which AI is best?" The better question is "which tier does this workflow belong in?"

That's a different conversation. It depends on volume, data sensitivity, regulatory exposure, latency requirements, fine-tuning needs, and how much control you need over upgrades and behavior. Once you know the tier, the shortlist of options becomes obvious. Skip that step and you'll either overpay on API tokens for workloads that should be self-hosted, or you'll over-engineer self-hosting for workloads that should just hit an API.

This is exactly the kind of structural decision we work through in an AI Operating Audit. Not a model bake-off. A clear map of which workflows belong in which tier, what that costs over a real time horizon, and where the lock-in risks are. If you want to see how we think about it across a full operating model, the HIP OS platform is built around exactly this kind of decision architecture.

Gemma 4 isn't a gift. It's a position. Read the move correctly and you'll make better ones of your own.

Infographic

Frequently Asked Questions

- Why did Google release Gemma 4 as open-weight?

- Not generosity. Google is the only major lab that can compete in both the closed API tier and the open self-hosted tier, because it owns the cloud, the TPUs, and Android. Gemma captures workloads Gemini was never going to win, then routes them onto Google infrastructure.

- When does self-hosting an open-weight model actually make sense?

- Volume. A startup spending $2,000 a month on API calls will stay closed because convenience wins. A company spending $2 million a month should look at self-hosting seriously. At scale, open weights can run 10 to 100 times cheaper than per-token APIs.

- Why can't OpenAI do what Google did with Gemma?

- OpenAI doesn't have a cloud, its own chips at scale, or an Android. The model is the business. Give it away and there's nothing left to sell. They released GPT-OSS under pressure, but kept it a tier below frontier and shipped GPT-5 closed two days later.

- Why does the Chinese open-weight wave matter to Western enterprises?

- Qwen, DeepSeek, Moonshot, and Z.AI now rival GPT-5 and Claude in real workloads. For a Western enterprise wanting to self-host, the best technical option was starting to look Chinese. That's a geopolitical, procurement, and national security problem at the same time. Gemma 4 plants a U.S.-built flag in that space.

- How should leadership teams decide between closed APIs and open-weight self-hosting?

- Stop asking which AI is best. Ask which tier each workflow belongs in. The decision depends on volume, data sensitivity, regulatory exposure, latency, fine-tuning needs, and control over upgrades. Once you know the tier, the shortlist becomes obvious.

- Does Gemma cannibalize Gemini?

- No. Gemma captures self-hosted workloads Gemini was never going to win, while every Gemma benchmark win reinforces Gemini's reputation. The free model markets the paid one, and developers fluent in Google's stack today write procurement recommendations in three years.