The SaaSpocalypse: Stop Selling Shovels, Sell Holes

Key Takeaways

- On February 3, 2026, the S&P 500 Software Index fell 13% in a single day. The market finally priced what operators have felt for two years: when an agent does the work of ten people, you stop paying for ten seats.

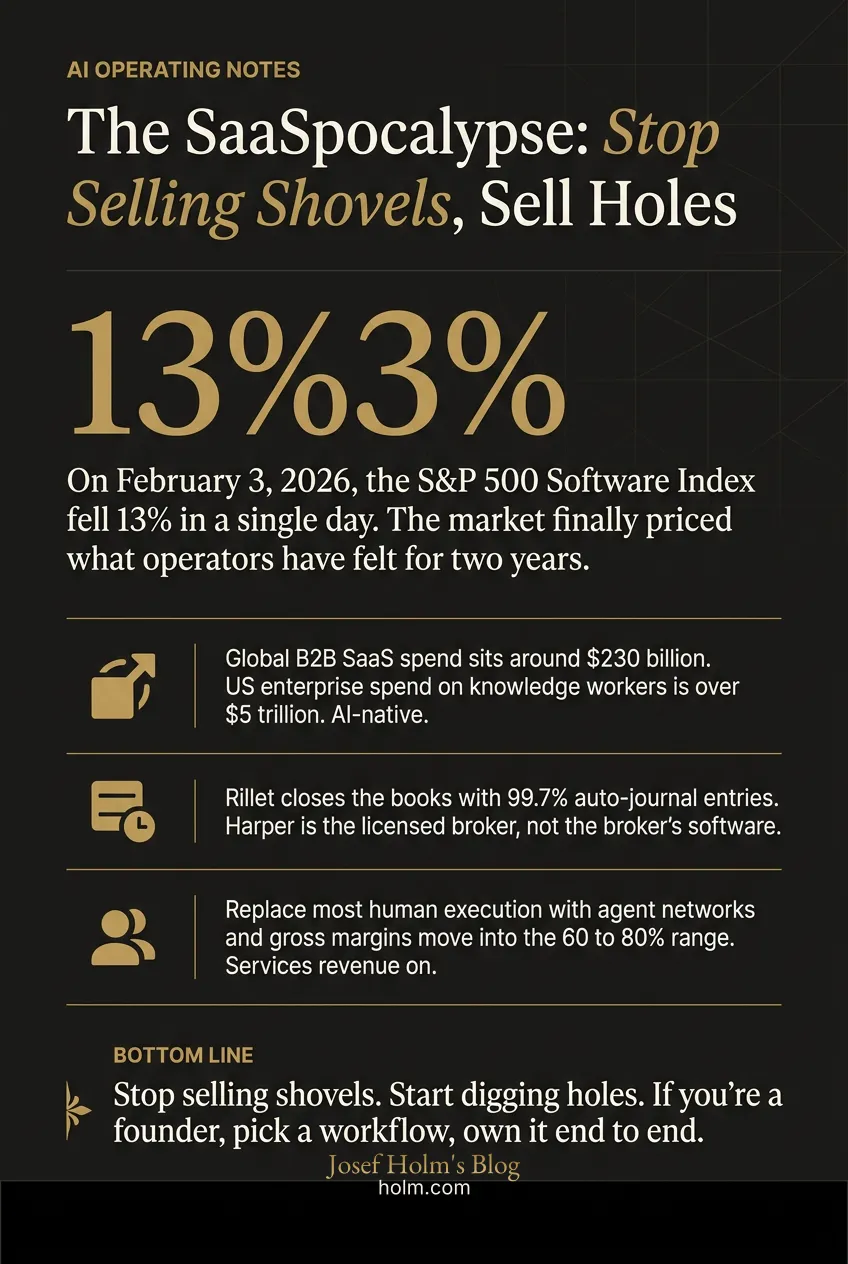

- Global B2B SaaS spend sits around $230 billion. US enterprise spend on knowledge workers is over $5 trillion. AI-native companies are going after the work, not the tooling around the work.

- Rillet closes the books with 99.7% auto-journal entries. Harper is the licensed broker, not the broker's software. Anterior runs prior auths at 99.24% accuracy. None of them charge per seat. They charge for the outcome.

- Replace most human execution with agent networks and gross margins move into the 60 to 80% range. Services revenue on software economics. That's the unlock VCs ignored for thirty years.

- Stop selling shovels. Start digging holes. If you're a founder, pick a workflow, own it end to end, price the outcome. If you're an operator, stop buying tools and start buying work.

The SaaSpocalypse Is Here: Why the Next Decacorns Will Sell Work, Not Shovels

On February 3, 2026, the S&P 500 Software Index fell 13% in a single day. Worst day on record. The market finally put a number on what most operators have felt for two years: when an AI agent can do the work of ten people, you stop paying for ten seats.

That's the whole story. Seat-based software is getting compressed in real time, and the winners of the next decade won't sell tools. They'll sell finished work.

I've been building software companies for three decades. Plenty of "this changes everything" moments turned out to be marketing. This one is different. The math is too clean to argue.

What actually broke on Black Tuesday?

Anthropic shipped Claude Cowork and Claude Code. OpenAI rolled out ChatGPT Agent Mode to the public. These aren't autocomplete features. They move around desktops, close tickets, and run multi-step workflows without a human in the loop for most of it.

The market saw what that means for per-seat and repriced an entire category overnight. Wall Street called it "seat compression." I'd call it the bill coming due.

For twenty years, B2B SaaS built valuations on one idea: charge per user, expand by pushing more users into the account. That model assumes humans are the unit of execution. Once the unit of execution is an agent, the seat is a rounding error.

Why is this shift so big economically?

Because the budgets in play are an order of magnitude larger.

Global B2B SaaS spending sits around $230 billion a year. US enterprise spending on knowledge workers is north of $5 trillion. The software industry has been fishing in the small pond while the big pond sat untouched.

Sequoia's Julien Bek put it cleanly in his March 2026 essay Services: The New Software. For every dollar spent on software, roughly six are spent on services to operate that software. Consultants. Outsourced teams. Agencies. Internal ops headcount. The tool was never the value. The work was.

AI-native companies are now going after the work directly. They're not selling the milkshake machine. They're selling the milkshake.

Copilot or autopilot? They're not the same business.

Here's where most founders get it wrong. Bolting an AI feature onto an existing SaaS doesn't make a company AI-native. It just makes the old model run a little faster.

A traditional agency with AI tools is still human-first. Humans run the workflow, AI helps them move quicker, headcount scales with revenue. Gross margins stay capped where services margins have always been capped.

An AI-native service company flips that. Software is the default workforce. Agents run the workflow end to end. Humans sit at the exception layer, handling strategy, brand judgment, final QA. Headcount stops scaling linearly with revenue. That's the unlock.

This is why Y Combinator put "AI-native service companies" at the top of its Request for Startups. They're not funding better tools. They're funding companies that absorb entire job functions.

Who is already winning?

This isn't theoretical. Look at what's already shipping:

Rillet is an AI-native ERP that closes the books on its own. It plugs into banks and billing tools and books 99.7% of journal entries without a human involved. They've raised $108.5 million from Sequoia, a16z, and ICONIQ. They don't charge per accountant. They charge for the close.

Anterior runs clinical prior authorizations in healthcare. Nurses used to spend hours parsing faxed medical records. Anterior's platform handles it with 99.24% clinical accuracy inside secure AWS environments and cuts manual review time by 75%.

Harper doesn't sell software to insurance brokers. Harper is the licensed broker. One of their brokers can manage up to 1,000 clients. Industry average is 20 to 30. They cut policy placement from weeks to under 24 hours.

Astraea runs clinical trial biometrics with multi-agent networks. They handle SDTM mapping, ADaM transformations, and produce CDISC-ready outputs at 100%. They compress reporting windows by 30 to 50%.

See the pattern? None of these companies sell access. They sell completed outcomes inside regulated, high-value workflows. That's the playbook.

What does this do to margins and?

Classic services businesses were un-investable at venture scale because gross margins capped below 30%. Too much human labor sat in the delivery cost. VCs ignored the category for thirty years.

AI-native services rewrite the math. Replace most human execution with agent networks and your marginal cost of delivery collapses to inference and token spend. Gross margins move into the 60 to 80% range. Software economics on a services revenue base.

follows margin. The seat is dying. Recent buyer studies show 86% of enterprise buyers now prefer usage or outcome-based over seat licenses. A few models are emerging:

- Platform plus agent fee. Base subscription plus usage charges for agent activity.

- Platform plus outcome bonuses. Predictable base fee with performance tied to specific results: a contract closed, an authorization approved, a ticket resolved.

- Pure outcome. You pay for the work itself. Intercom's Fin charges $0.99 per resolved support issue. No seats. No subscription. Just work done.

Anyone still per seat in 2027 will look like the firms selling boxed software in 2012.

What does this mean if you're running a mid-market or PE-backed business?

Two things matter right now, and most leadership teams are getting both wrong.

Your existing software stack is about to get reshuffled. Seat-based vendors will either reprice toward outcomes or get displaced by AI-native competitors that absorb the function entirely. Your CFO should be modeling that exposure now, not in 2027.

Your services spend is the bigger opportunity. Look at where you're paying agencies, consultants, BPOs, and large internal ops teams to run repeatable workflows. That's where AI-native vendors will arrive first, and where the margin recapture is largest. Companies that move early will retire entire cost centers. The ones that wait will watch competitors do it first.

This is the kind of repositioning we work on inside an AI readiness note. Not a tooling exercise. A structural look at which functions still need humans, which need orchestration, and which should be replaced with an outcome contract from an AI-native vendor.

For companies in the middle of an integration or post-close transition, the question is sharper. You're already rebuilding the org. Build it for the agent-first model, not the seat-first one. That's most of what we do inside implementation notes right now.

Is SaaS dead?

No. The framing is wrong.

Simple software tools are commoditizing because the cost to build them has collapsed to near zero. Any decent founder with Claude Code can ship in a weekend what took a team six months in 2022. The moat around generic SaaS is gone.

But software that orchestrates agent networks, runs regulated workflows, and stands behind delivered outcomes is worth more than ever. The moat just moved. It's no longer "we have a feature you don't." It's "we own the workflow end to end and we're accountable for the result."

That's a deeper moat. Harder to build. Worth more when it works.

Stop selling shovels. Start digging holes.

The customer never wanted the shovel. They wanted the hole. SaaS spent twenty years selling shovels because shovels were the best we could build. That constraint is gone.

The next generation of decacorns will take a high-value, repeatable knowledge-work function, wrap it in a reliable agent network, and sell the completed outcome with a single point of accountability. Books closed. Authorizations approved. Policies placed. Trials reported.

If you're a founder, stop building features. Pick a workflow, own it end to end, price the outcome.

If you're an operator, stop buying tools. Start buying work.

The shift is already priced into public markets. The only question is whether you're on the right side of it inside your own business.

Infographic

Frequently Asked Questions

- What is the SaaSpocalypse?

- The repricing of seat-based software once AI agents can run workflows without humans in the loop. On February 3, 2026, the S&P 500 Software Index fell 13% in a single day. That's the market putting a number on it. When agents do the execution, the seat becomes a rounding error.

- What is an AI-native service company?

- A company that uses software as its default workforce. Agents run the workflow end to end, humans handle exceptions, strategy, and final QA. Headcount stops scaling linearly with revenue. That's different from an agency that bolted AI onto a human-first delivery model.

- Is SaaS dead?

- No. Simple tools are commoditizing because anyone with Claude Code can ship in a weekend what took a team six months in 2022. But software that orchestrates agent networks, runs regulated workflows, and stands behind delivered outcomes is worth more than ever. The moat moved from features to end-to-end accountability.

- How should change away from seats?

- Three models are emerging. Platform plus agent usage fee. Platform plus outcome bonuses tied to specific results. Pure outcome like Intercom's Fin at $0.99 per resolved ticket. 86% of enterprise buyers now prefer usage or outcome-based over seat licenses.

- What should a mid-market or PE-backed business do right now?

- Two things. Model your seat-based vendor exposure before 2027, because they'll reprice or get displaced. And look at your services spend (agencies, consultants, BPOs, internal ops) for repeatable workflows where AI-native vendors can absorb the function and you can retire entire cost centers.

- Why are gross margins so different for AI-native services?

- Classic services businesses were capped below 30% gross margins because human labor sat in the delivery cost. Replace most of that execution with agent networks and your marginal cost collapses to inference and token spend. Margins move into the 60 to 80% range. Software economics on a services revenue base.